Understanding your car insurance policy is essential to ensure you are adequately covered and to avoid surprises when you need to make a claim. Car insurance can be confusing, with numerous terms and conditions, coverage types, and exclusions. However, by breaking down your policy into key sections, you can gain a clearer understanding of what’s covered and how your policy works. In this article, we’ll guide you through how to read and understand your car insurance policy step-by-step.

1. Start with the Declaration Page

The declaration page, often referred to as the “dec page,” is the first page of your policy. This page summarizes the most important details of your coverage, including the types of coverage, policy limits, and vehicle information.

Key details on the declaration page include:

- Policyholder Information: Your name, address, and contact details.

- Vehicle Information: Details about the car or cars covered, including the make, model, year, VIN (Vehicle Identification Number), and any additional drivers covered.

- Coverage Types: The types of coverage included in your policy (e.g., liability, comprehensive, collision, uninsured motorist, etc.).

- Policy Period: The start and end date of your coverage period.

- Premium: The amount you pay for your car insurance policy, often listed as an annual or semi-annual amount.

The declaration page is the easiest place to get a quick overview of your coverage, and it will help you understand the basic aspects of your insurance policy.

2. Review the Types of Coverage

Your car insurance policy may offer several types of coverage, each designed to protect you in different scenarios. The two primary categories of coverage are liability and non-liability (optional) coverage. Here’s a breakdown of the most common types:

- Liability Coverage: This covers damages you cause to other people or property in an accident. It typically includes:

- Bodily Injury Liability: Covers medical expenses, lost wages, and pain and suffering for the other party involved in an accident you caused.

- Property Damage Liability: Covers repairs or replacement costs for the other person’s property, such as their vehicle, fence, or building, that you damaged in an accident.

- Collision Coverage: Covers damage to your vehicle in the event of a collision, regardless of fault. This is optional but highly recommended, especially for new or expensive cars.

- Comprehensive Coverage: Protects your car against non-collision events such as theft, vandalism, fire, natural disasters, or hitting an animal. It’s optional but recommended if your car is valuable or in an area prone to such risks.

- Uninsured/Underinsured Motorist Coverage: Covers your medical bills and property damage if you are in an accident with a driver who has no insurance or insufficient coverage.

- Medical Payments Coverage: Pays for medical expenses for you and your passengers in the event of an accident, regardless of who is at fault.

- Personal Injury Protection (PIP): Similar to medical payments coverage but more extensive, PIP may also cover lost wages, rehabilitation costs, and other non-medical expenses incurred due to an accident.

- Roadside Assistance: Offers services such as towing, flat tire changes, and fuel delivery if you break down.

Each type of coverage will have its own set of limits, deductibles, and exclusions. Make sure to carefully review each coverage option listed in your policy to understand the extent of protection provided.

3. Understand Your Policy Limits

The policy limit refers to the maximum amount your insurance company will pay for a covered loss. These limits can vary depending on the type of coverage and the policy you’ve chosen. They are typically listed as two numbers, such as 100/300/50 or 250/500.

Here’s what these numbers typically represent:

- 100 or 250: The maximum amount the policy will pay for bodily injury per person involved in an accident.

- 300 or 500: The maximum amount the policy will pay for bodily injury for all parties involved in the accident (total per accident).

- 50 or 100: The maximum amount the policy will pay for property damage in an accident.

For example, a 100/300/50 policy means your insurer will pay up to $100,000 per person for bodily injury, up to $300,000 total for bodily injury in an accident, and up to $50,000 for property damage.

Make sure the limits on your policy reflect the value of your assets. Higher limits offer more protection but also come with higher premiums.

4. Check the Deductibles

A deductible is the amount you pay out of pocket before your insurance coverage kicks in. It applies to certain types of coverage, such as comprehensive and collision.

For example, if you have a $500 deductible on collision coverage and you’re in an accident that causes $2,000 worth of damage, you’ll pay the first $500, and your insurance company will cover the remaining $1,500.

Deductibles can vary depending on the coverage, and the higher your deductible, the lower your premium typically will be. However, you’ll need to be prepared to pay the deductible out of pocket if you need to file a claim. Make sure you choose a deductible amount that fits your budget.

5. Know the Exclusions

Every car insurance policy has exclusions—situations or events that are not covered by your policy. Common exclusions can include:

- Intentional Damage: If you cause an accident on purpose, your insurance will not cover the damage.

- Racing: Most policies exclude coverage if you’re involved in a race or similar high-speed event.

- Driving Under the Influence: If you’re caught driving while intoxicated or under the influence of drugs, your policy likely won’t cover the damages.

- Unlicensed Drivers: If the driver of your car does not have a valid driver’s license, insurance may not cover the accident.

Understanding your policy’s exclusions is important so you can avoid situations where your claim may be denied.

6. Pay Attention to Policy Endorsements and Riders

Endorsements (or riders) are amendments to your standard policy that either add extra coverage or modify existing coverage. These are typically used to tailor the policy to your specific needs. For example, you may add coverage for custom parts, like aftermarket wheels or stereo systems, if they’re not covered by the standard policy.

Common endorsements include:

- Rental Car Coverage: Pays for a rental car while your vehicle is being repaired after an accident.

- Gap Insurance: Covers the difference between what you owe on your car loan and the car’s actual cash value if your car is totaled.

- Custom Equipment Coverage: Covers aftermarket parts and accessories installed in your vehicle.

Make sure to review any endorsements and riders to fully understand what additional coverage you have and whether any extra costs are associated with them.

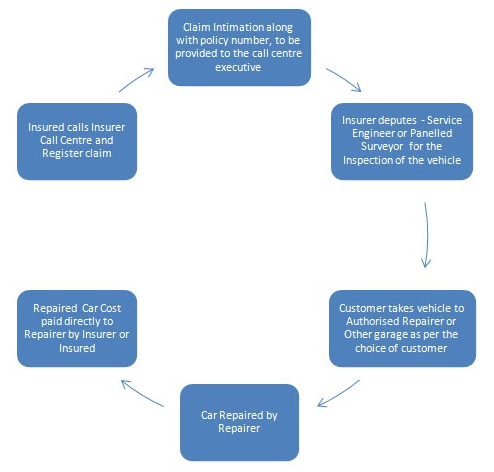

7. Examine the Claims Process

Your car insurance policy should also outline the steps you need to follow if you need to file a claim. This includes the information you’ll need to provide, such as the police report (if applicable), details of the accident, and photographs of the damage.

The claims process section may also specify how soon after an accident you must notify your insurer and any deadlines for filing a claim. Understanding this section of your policy can save you time and frustration if you ever need to make a claim.

8. Review the Policy Renewal Process

Car insurance policies typically last for one year, after which they need to be renewed. When reviewing your policy, check the renewal process and whether your premium will change at the time of renewal. Insurance companies may increase your premiums based on claims made during the previous policy period or changes in your driving record.

It’s a good practice to review your coverage every year to make sure it still meets your needs. If necessary, shop around to compare rates and ensure you’re getting the best value for your coverage.

Conclusion

Reading and understanding your car insurance policy is crucial to ensuring that you have the appropriate coverage for your needs. By carefully reviewing the declaration page, understanding the different types of coverage, and knowing your policy’s limits, deductibles, and exclusions, you can make sure you’re adequately protected. Be sure to ask your insurance provider for clarification if you have any questions about your policy, and regularly review your coverage to ensure it aligns with your evolving needs. By staying informed, you can avoid surprises and have peace of mind when you’re on the road.