In the complex world of health insurance, one option that often gets overlooked is COBRA insurance. The Consolidated Omnibus Budget Reconciliation Act, more commonly known as COBRA, offers individuals and families the ability to continue their health insurance coverage after experiencing certain life events that would otherwise terminate their benefits. This article explores COBRA insurance, how it works, its eligibility requirements, and its pros and cons.

What is COBRA Insurance?

COBRA is a federal law passed in 1985 that allows employees and their families to continue their group health insurance coverage after a qualifying event. These qualifying events include situations such as job loss, reduction in working hours, divorce, or the death of the covered employee. Prior to the passing of COBRA, workers and their families often found themselves without health insurance once they lost their employment, leaving them vulnerable to expensive medical costs.

Under COBRA, individuals who lose their job or experience another qualifying event can extend their health coverage for a specific period, typically up to 18 months, though in some cases, it can extend up to 36 months. The law applies to employers with 20 or more employees and to group health plans offered by private-sector employers and state and local governments.

How Does COBRA Insurance Work?

When an employee becomes eligible for COBRA, they are given the opportunity to continue the same health insurance coverage they had while employed. The insurance will remain the same as the coverage the employee received as part of their job benefits, which means the same doctors, hospitals, and medications are covered.

However, there is one important difference: the cost of the health insurance. Under COBRA, the individual is responsible for paying the full premium amount. While employed, workers typically only pay a portion of their health insurance premium, with their employer covering the rest. But under COBRA, the employee must cover the full premium, which includes both their portion and the employer’s portion. Additionally, COBRA allows the employer to charge a 2% administrative fee, meaning the total cost can sometimes be higher than what the employee was paying while employed.

Once an individual elects COBRA coverage, they have up to 60 days to decide whether to enroll in the plan. If they choose to enroll, coverage will begin immediately after the qualifying event occurs. However, it’s important to note that COBRA coverage is not automatic; individuals must proactively elect to continue their benefits.

Eligibility for COBRA Insurance

To qualify for COBRA coverage, certain conditions must be met:

- Employer Size: COBRA applies to employers with 20 or more employees who offer a group health plan. Smaller employers are not obligated to provide COBRA benefits, although some states have “mini-COBRA” laws that extend similar benefits to smaller businesses.

- Qualifying Events: Employees (and their dependents) may qualify for COBRA coverage after experiencing a qualifying event. These include:

- Job loss (voluntary or involuntary, except in cases of gross misconduct)

- Reduction in work hours (which results in loss of health coverage)

- Divorce or legal separation from the employee

- Death of the employee, leaving the spouse and dependent children without coverage

- Loss of dependent status (e.g., a child turning 26 and no longer eligible for coverage under a parent’s plan)

- Notice Requirement: Employers must provide a notice of COBRA rights to employees and their families when they experience a qualifying event. It is crucial that the individual or their family members notify the employer or plan administrator within 60 days of a qualifying event (such as divorce or a child reaching the age limit) to ensure they don’t lose their right to COBRA coverage.

Duration of COBRA Coverage

COBRA coverage typically lasts for 18 months, but there are exceptions. The length of coverage can vary depending on the nature of the qualifying event and the individual’s specific circumstances:

- 18 months: For employees who experience a job loss or reduction in work hours, coverage is available for up to 18 months.

- 29 months: If a qualified beneficiary is disabled, they may be eligible to extend their COBRA coverage for up to 29 months, provided they meet certain criteria and notify the plan administrator within the first 60 days of receiving COBRA benefits.

- 36 months: Coverage can be extended up to 36 months for dependents who lose their coverage due to the employee’s death, divorce, or legal separation.

It’s important to note that COBRA coverage ends early if the individual becomes eligible for other group health insurance coverage, such as through a new employer or a spouse’s plan.

Cost of COBRA Insurance

While COBRA is a lifeline for many who are temporarily without health coverage, the cost can be a significant burden. Under COBRA, individuals must pay the entire premium for their health plan, which includes the amount that was previously covered by their employer. Additionally, employers are allowed to charge a 2% administrative fee.

For many individuals, this means paying hundreds or even thousands of dollars per month for health insurance. Depending on the type of plan, the cost can be prohibitive for those who are already facing financial challenges, such as those who have lost their job.

Pros and Cons of COBRA Insurance

Pros

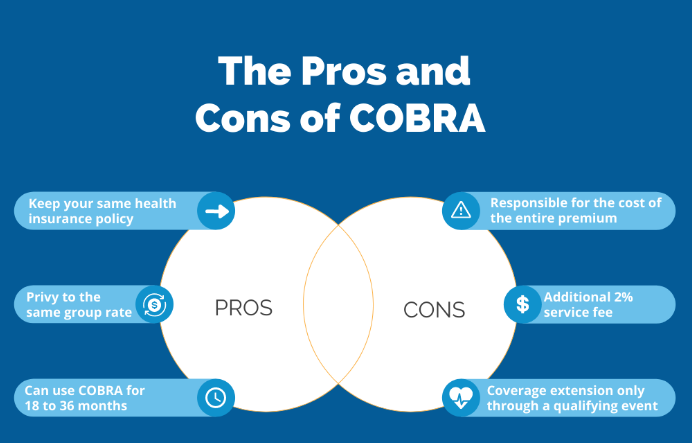

- Continuity of Coverage: The biggest advantage of COBRA is that it allows individuals to maintain the same health insurance coverage they had while employed. This means they can continue seeing the same doctors and use the same healthcare providers without any interruptions.

- No Waiting Period: Unlike some private insurance options, COBRA coverage begins immediately after the qualifying event, so there is no waiting period for coverage.

- Protection for Families: COBRA extends coverage not only to the employee but also to their family members. This ensures that spouses and children can continue to receive healthcare benefits even after a life event like divorce or the death of the covered employee.

Cons

- Cost: The most significant downside of COBRA is its cost. Since individuals are responsible for the full premium, it can be prohibitively expensive, especially for those who are already facing financial difficulties due to job loss or other reasons.

- Limited Duration: COBRA coverage is temporary, and while it can be extended in certain situations, it does not offer a long-term solution for health insurance.

- Administrative Burden: Managing COBRA enrollment and payments can be complex, and failure to adhere to deadlines can result in the loss of coverage.

Alternatives to COBRA

For many, COBRA may not be a sustainable long-term option due to its high cost. Fortunately, there are alternatives:

- Marketplace Insurance: The Health Insurance Marketplace (created under the Affordable Care Act) offers individual health plans that may be more affordable than COBRA, especially if you qualify for subsidies based on your income.

- Medicaid: If your income is low enough, you may qualify for Medicaid, a state and federal program that provides health coverage for individuals and families with limited income.

- Spouse’s Plan: If you’re married, you may be able to join your spouse’s health insurance plan, which may offer a more affordable option.

Conclusion

COBRA insurance provides essential coverage for those who experience life changes that result in the loss of their employer-sponsored health plan. It allows individuals and their families to maintain health coverage during a challenging time, giving them peace of mind as they navigate their next steps. However, the cost and temporary nature of COBRA coverage can make it a less than ideal long-term solution for many people. It’s crucial to evaluate all available options and choose the plan that best suits your financial and healthcare needs.