Health insurance is one of the most significant benefits many people have while employed. However, when you lose your job, it can be a daunting task to figure out how to maintain your health insurance coverage. This is where COBRA insurance comes into play. The Consolidated Omnibus Budget Reconciliation Act (COBRA) is a federal law that allows employees and their families to continue their employer-sponsored health insurance for a limited period after losing their job or experiencing other qualifying life events.

In this article, we will explore what COBRA insurance is, how it works, its eligibility requirements, the costs associated with it, and the pros and cons of continuing coverage under COBRA.

What is COBRA Insurance?

COBRA stands for the Consolidated Omnibus Budget Reconciliation Act, a law passed in 1985 that provides workers and their families the ability to continue their health insurance coverage after leaving their job or experiencing certain life events. The law applies to group health plans maintained by employers with 20 or more employees, and it mandates that employers offer continued health coverage to employees who experience a loss of benefits due to various circumstances, including job loss, reduction in work hours, or other qualifying events.

COBRA allows individuals to retain the same health insurance coverage they had while employed, meaning they can keep their doctors, treatments, and prescription medications. However, while COBRA can provide a safety net for those who find themselves without health insurance, it is essential to understand the details of how it works.

How COBRA Works

When you lose your job or experience a life event that qualifies you for COBRA coverage, the process typically unfolds in several steps:

- Notification from Employer:

- When your employment ends or you experience a qualifying event (such as divorce or the death of a covered spouse), your employer is required to notify the health insurance plan administrator.

- Within 14 days of the event, your employer must send you a notice informing you of your right to elect COBRA coverage.

- Election Period:

- After receiving the notification, you will have a 60-day window to decide whether you want to continue your coverage under COBRA.

- If you don’t elect COBRA coverage within the 60-day period, you forfeit your right to continue your employer-sponsored health plan.

- Coverage:

- Once you elect COBRA, you can continue your health insurance coverage under the same terms you had as an active employee. This includes medical, dental, and vision insurance (if those benefits were included in your original plan).

- COBRA coverage can last for up to 18 months in most cases, but it may be extended for up to 36 months for certain qualifying events (e.g., disability or divorce).

- Premium Payments:

- Under COBRA, you are responsible for paying the full premium for the insurance coverage. This includes the portion you previously paid while employed and the portion your employer used to contribute to your premiums, plus a 2% administrative fee.

- Although this can make COBRA more expensive than your previous premium costs, it provides you with the ability to maintain the same insurance coverage.

- Termination of COBRA:

- COBRA coverage will end if you fail to pay the premiums, the employer stops offering health insurance, or you become eligible for another group health plan (such as through a new employer or spouse).

- If your employment ends due to gross misconduct, you are not eligible for COBRA coverage.

Eligibility for COBRA

COBRA coverage is available to employees, their spouses, and dependent children who were covered under the employer’s health plan. However, there are certain eligibility requirements and qualifying events for COBRA:

Qualifying Events for Employees:

- Job loss (voluntary or involuntary) that results in the loss of health insurance

- Reduction in work hours that makes you ineligible for health coverage

- Disability (if you are deemed disabled by the Social Security Administration, you may be eligible for a 29-month extension)

- Retirement (as long as the employer continues to offer health insurance to retirees)

Qualifying Events for Family Members:

- Spouse’s job loss or reduction in hours

- Divorce or legal separation from the covered employee

- Death of the covered employee

- Loss of dependent status (children aging out of the plan at age 26)

It’s important to note that COBRA is only available to employees who worked for employers with 20 or more employees. Employees of smaller businesses are not eligible for COBRA, but they may have other options, such as purchasing insurance through the Health Insurance Marketplace.

Costs of COBRA Insurance

One of the major drawbacks of COBRA insurance is the cost. Under COBRA, the individual must pay the full premium for the health insurance plan, which includes both the employee’s and employer’s contributions. Additionally, there may be a 2% administrative fee added to the total cost.

Example of Costs:

- Let’s say your employer’s contribution was $300 per month, and your share of the premium was $200 per month. Under COBRA, you will be required to pay the full premium ($500) plus the 2% administrative fee. Therefore, the total cost would be approximately $510 per month.

- The cost of COBRA insurance can be prohibitively high for some individuals, especially those who lose their job and are already facing financial hardship.

Pros and Cons of COBRA Insurance

While COBRA offers a way to continue coverage after losing a job or experiencing a life event, there are both advantages and disadvantages to consider.

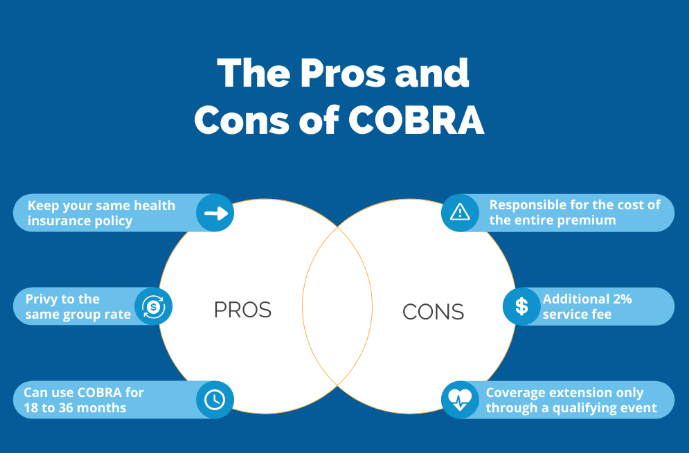

Pros of COBRA:

- Continuity of Coverage: COBRA allows you to maintain the same health insurance plan you had while employed, which means you don’t have to find a new provider or switch doctors. This continuity of care can be especially important if you have ongoing medical needs or are undergoing treatment.

- No Medical Underwriting: COBRA insurance guarantees coverage regardless of any pre-existing conditions. This is particularly beneficial for individuals who may have health conditions that could make it difficult to obtain individual insurance coverage.

- Family Coverage: COBRA not only covers the individual who lost their job, but it can also extend coverage to their spouse and dependent children, which can be a relief for families who need to maintain health insurance for multiple members.

Cons of COBRA:

- Cost: The most significant drawback of COBRA is the cost. You are responsible for paying the full premium, which may be higher than the amount you were paying as an employee. For many people, the cost of COBRA can be a financial burden.

- Temporary Coverage: COBRA coverage is temporary, typically lasting only 18 months, though it may be extended in certain cases. This means that you’ll eventually need to find an alternative source of coverage, which can be stressful if you’re still unemployed or underinsured.

- Limited Availability: COBRA is only available to employees of businesses with 20 or more employees, so those working for smaller employers may not have access to this option. Additionally, if your employer discontinues the group health plan, COBRA coverage may not be available.

Alternatives to COBRA

If COBRA is too expensive or not an option for you, there are several alternatives to consider:

- Health Insurance Marketplace: You may qualify for subsidies under the Affordable Care Act (ACA) if your income is below a certain threshold. You can purchase a health insurance plan through the Health Insurance Marketplace during a Special Enrollment Period triggered by the loss of your job.

- Medicaid: If you lose your job and your income drops significantly, you may be eligible for Medicaid, which provides free or low-cost health coverage for low-income individuals and families.

- Spouse’s Health Insurance: If your spouse has access to employer-sponsored health insurance, you may be able to join their plan as a dependent.

Conclusion

COBRA insurance provides a valuable option for individuals who lose their job or experience certain life events, offering the ability to continue employer-sponsored health coverage for a limited period. However, it comes with costs and limitations, including the requirement to pay the full premium. When considering COBRA, it’s essential to weigh the cost of coverage against the benefits of continuity of care and no medical underwriting.

If COBRA is not a viable option, there are other health insurance alternatives available, such as the Health Insurance Marketplace, Medicaid, or a spouse’s plan. Ultimately, understanding your options and acting quickly will ensure that you maintain the health coverage you need during a time of transition.